Saving for retirement is one of the most important financial strategies of your lifetime. But people who use traditional retirement accounts have limited investment options—typically stocks, bonds, and mutual funds. While those investments have their place, stock market volatility is a concern. If you want to take a more active role in building your retirement wealth, offset stock market losses, and diversify into markets you understand—a self-directed IRA (SDIRA) might be the answer.

This comprehensive guide walks you through what a self-directed IRA is, how it works, who it’s for, the benefits and risks, and what rules you need to follow to stay compliant. Whether you’re just starting to explore alternative assets or you’re a seasoned investor looking to diversify, this article will equip you with everything you need to know.

What Is a Self-Directed IRA?

A self-directed IRA is a type of retirement account that allows you to invest in a broader range of assets than a conventional IRA permits. The account structure and rules are the same as other IRAs. The main difference is in who’s calling the shots. With an SDIRA, you (the account holder) choose the investments and can use real estate, private equity, startups, cryptocurrency, gold, and other alternative investments to build retirement wealth. You and you alone make decisions regarding how your retirement funds are spent.

Who Uses Self-Directed IRAs—and Why?

Self-directed IRAs are used by a wide range of investors:

- New investors who want to diversify early and explore tangible assets like real estate

- Experienced investors who have industry knowledge—say, in private lending or startups—and want to leverage that expertise

- Small business owners, entrepreneurs, and freelancers who want more control over retirement accounts like SEP and SIMPLE IRAs or solo 401(k)s

- Mission-driven investors who want their retirement savings to reflect personal values—such as sustainable farming, affordable housing, or renewable energy

In short, people use SDIRAs because they want freedom, flexibility, and control. These accounts put you in the driver’s seat to build a more customized and potentially resilient retirement portfolio.

What Are the Benefits of a Self-Directed IRA?

Self-directed IRAs offer unique advantages, including:

- Wider investment choices: You can invest in alternative assets—a variety of choices not available through conventional retirement plans.

- Diversification: SDIRAs help spread risk beyond public markets.

- Tax advantages: You retain the tax-deferred or tax-free benefits of traditional or Roth IRAs while investing in alternative assets.

- Personalized strategy: Invest in what you know—whether that’s local real estate, private lending, or small businesses.

- Potential for higher returns: While riskier, some alternative investments (like real estate)may outperform conventional markets over time.

What Can You Invest in with an SDIRA?

While the full list is extensive, here are some of the most popular alternative assets that investors hold in a self-directed IRA:

- Real estate (residential, commercial, land)

- Private lending and promissory notes

- Private equity and startups

- Precious metals (e.g., gold, silver)

- Cryptocurrency

- Tax liens and deeds

- Oil and gas interests

- Limited partnerships (LPs) and LLCs

Each asset comes with its own set of rules and considerations, so it’s crucial to do your research before diving in.

What Can’t You Invest In?

The IRS’s list of things you can’t invest in with a self-directed IRAs is surprisingly short, but it’s important to be aware of these restrictions to avoid costly mistakes.

Prohibited Investments

- Collectibles, including artwork, antiques, rugs, gems, stamps, coins (with a few exceptions), alcoholic beverages, and other tangible personal property considered collectible under IRS guidelines

- Life insurance contracts, including whole life or variable life policies

All other investment types are generally allowed, as long as they do not involve prohibited transactions or disqualified persons. This broad flexibility is what makes SDIRAs so attractive—but also why due diligence is essential. Even allowable investments can lead to compliance issues if they aren’t structured properly.

Types of Accounts That Can Be Self-Directed

Self-direction isn’t just for one type of IRA—it can be applied to nearly any tax-advantaged account.

Traditional IRA

Contributions may be tax-deductible, and the investment grows tax deferred. You pay taxes on withdrawals in retirement. Traditional IRAs are ideal for individuals who expect to be in a lower tax bracket in retirement and want to reduce their current taxable income.

Roth IRA

You contribute after-tax dollars, and distributions in retirement are tax free. A Roth is beneficial for those expecting to be in a higher tax bracket later or looking for long-term tax-free growth.

SEP IRA

Designed for self-employed individuals or small business owners, SEP IRAs offer higher contributions than traditional or Roth IRAs.

SIMPLE IRA

The SIMPLE IRA is another retirement plan for small businesses, with lower contribution limits than SEPs, but offers both employer and employee contributions.

Solo 401(k)

This is a powerful plan for self-employed individuals with no full-time employees. A solo 401(k) allows for both employee and employer contributions as well as higher annual contributions and catch-up amounts than IRAs.

Health Savings Account (HSA)

HSAs allow tax-free growth of funds for health care expenses you need to cover now and in retirement. Leftover funds roll over year-to-year, and after the age of 65, you can use that money for anything without penalty.

Coverdell Education Savings Account (ESA)

ESAs provide a way to build tax-free income for educational expenses. Parents and others can make contributions to benefit a child, and you can roll over unused funds into a family member’s name.

IRS Rules and Prohibited Transactions for Self-Directed IRAs

While SDIRAs offer flexibility, they also come with specific rules. The IRS strictly regulates how you invest and with whom.

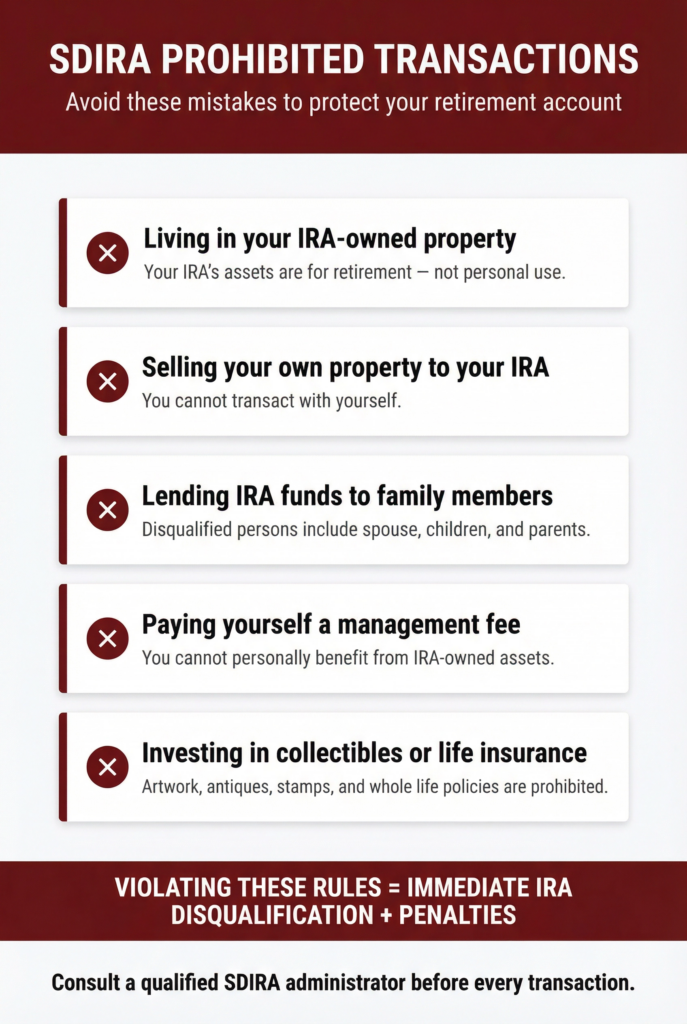

One of the most important things to understand is the concept of prohibited transactions—certain actions that are off-limits.

Examples of Prohibited Transactions:

- Purchasing a rental property with your IRA and living in it, or letting your family stay there

- Selling property you already own to your IRA

- Using your IRA funds to lend money to your children

- Paying yourself a management fee from your IRA-owned business or rental property

- Investing in collectibles or life insurance

Violating these rules can result in the disqualification of your IRA and the immediate taxation of the account’s assets, plus penalties.

Who Are Disqualified Persons?

To prevent conflicts of interest, the IRS prohibits your IRA from transacting with certain people or entities, known as disqualified persons:

- You (the account holder)

- Your spouse

- Your children, grandchildren, and their spouses

- Your parents and grandparents

- Fiduciaries (including your plan administrator)

- Any entity (corporation, LLC, etc.) that is 50% or more owned or controlled by a disqualified person

These restrictions are in place because your retirement funds are reserved for your future and not meant for personal gain today.

Risks of Self-Directed Investing

Self-directed investing offers freedom—but it also comes with risks:

- Lack of liquidity: Some alternative investments can’t be easily sold.

- Market and asset risk: Although alternative asset performance isn’t necessarily dictated by the stock market, they can still lose value just like any investment.

- Scams and fraud: SDIRA investors are sometimes targeted because of their autonomy and lack of third-party oversight.

- Oversight and due diligence: You’re in control and must research, verify, and vet every opportunity.

The Importance of Due Diligence

When investing through an SDIRA, you are in charge of evaluating every opportunity. Unlike traditional retirement plans, where investment options are pre-screened by a brokerage firm or financial advisor (who also have a fiduciary responsibility), self-directed investing puts the onus on you to assess the risks, legitimacy, and potential returns of each asset.

Due diligence means thoroughly vetting an investment before your IRA funds are committed. That means verifying property values, checking business financials, understanding the terms of a private loan, and asking tough questions about risk and reward.

This process isn’t just a good idea—it’s essential. Many alternative investments are less regulated, less transparent, and far less liquid than stocks or bonds. Failing to properly investigate can result in capital loss, fraud exposure, or violations of IRS rules.

Consider hiring professionals to support your evaluation:

- Real estate agents or appraisers to provide market analysis and valuation

- CPAs or tax advisors to assess tax implications and entity structures

- Investment attorneys to review offering documents and flag legal risks

- Third-party due diligence firms (especially for private placements, syndications, or crowdfunding deals)

Never invest in something you don’t understand unless you have sought proper guidance. The power of an SDIRA is only as effective as your ability to use it wisely.

The Role of a Self-Directed IRA Administrator

Self-directed IRAs must be held by a self-directed custodian or administrator who is authorized to service retirement plans. This provider is responsible for administrative duties, including, but not limited to:

- Processing investment transactions based on your direction

- Providing annual tax reporting (Forms 5498 and 1099-R)

- Ensuring regulatory compliance for account structure (not investment quality)

However, administrators do not provide investment advice. Their role is to carry out your instructions and keep your account in good standing with the IRS.

Choose an administrator with:

- Transparent fee structures

- Experience with your preferred asset types

- Educational resources and client support

Building a Strategy with a Self-Directed IRA

One of the biggest mistakes new SDIRA investors make is focusing only on what they can invest in—real estate, private notes, crypto, etc.—without thinking through how those investments fit into their overall retirement strategy. A self-directed IRA isn’t just a novelty account for a one-off deal. Used wisely, it can be a long-term wealth-building vehicle that complements or even outperforms traditional holdings. That starts with asking the right questions.

To get started, define your strengths, weaknesses, and goals:

- What is your risk tolerance and investment timeline?

- Are you seeking cash flow, long-term growth, or both?

- How much of your retirement portfolio do you want to allocate to alternative assets?

- Will you need liquidity in the next few years, or are you comfortable with illiquid investments?

Answering these helps you create a diversified portfolio within your SDIRA that aligns with your personal financial goals. For example, someone nearing retirement might use an SDIRA to generate passive income through real estate or private lending. A younger investor might be more inclined to invest in early-stage startups or private equity with higher growth potential (and risk).

The beauty of self-direction is that you’re not locked into a one-size-fits-all solution. You can design your own path—as long as you stay compliant and act prudently.

Checkbook Control: What It Is and When It Makes Sense

Some investors choose to add another layer of flexibility to their SDIRA by forming an LLC that the IRA owns. This structure is often called a checkbook IRA, and it allows you to write checks to invest. The account holder (you) acts as manager of the LLC, which gives you direct access to your retirement funds through a dedicated business bank account established in the LLC’s name.

This setup can be helpful for active investors who need to act quickly—like placing a bid at a real estate auction, writing checks for investment expenses, or seizing time-sensitive opportunities. Instead of routing every transaction through your custodian, you manage the LLC’s checkbook and buying the investment yourself.

But this freedom comes with greater responsibility. You must follow IRS rules to the letter for both IRAs and LLCs, maintain proper records, and avoid any self-dealing. The IRS doesn’t give second chances on prohibited transactions—even if they happen by accident. You’ll incur penalties, taxation, or even disqualification of your retirement account’s tax-advantaged status.

Checkbook control isn’t for everyone, but when used appropriately and with proper guidance, it can be a powerful tool for experienced investors who want more transactional agility.

Is a Self-Directed IRA Right for You?

Self-directed IRAs offer an exciting opportunity to take control of your retirement savings. They empower you to go beyond the stock market and invest in what you know, what you believe in, and what you’re passionate about.

But remember, with that power comes responsibility. You must understand the rules, conduct your own due diligence, and stay compliant with IRS regulations.

For proactive investors with an appetite for alternative assets—and a willingness to put in the work—self-directed IRAs can be a powerful way to build long-term, tax-advantaged wealth on your own terms.

If you’re intrigued by the possibilities, the next step is to learn more about custodians, asset classes, and best practices for compliance. With the right strategy and support, your retirement plan doesn’t have to look like everyone else’s—and that might be your biggest financial advantage.

About Advanta IRA

Advanta IRA is widely recognized as one of the best self-directed IRA companies in the nation, empowering individuals to take full control of their retirement investing. With more than two decades of experience and over $3.5 billion in assets under administration, Advanta IRA combines industry expertise with a personalized approach that sets it apart from other administrators. Every client is paired with a dedicated account manager who guides them through each transaction, ensuring efficiency, accuracy, and peace of mind.

The firm’s team of professionals, including attorneys, MBAs, Certified IRA Services Professionals (CISPs), and Self-Directed IRA Professionals (SDIPs), provides exceptional knowledge and service in all aspects of self-directed retirement investing. Advanta IRA’s mission is simple: to make alternative investing accessible, transparent, and fully compliant while giving investors the freedom to choose assets that align with their goals and values.

Education is central to the company’s philosophy. Advanta IRA offers a robust library of free resources, including weekly webinars, podcasts, blogs, and case studies that help investors make informed decisions. Clients frequently praise the firm’s responsiveness and personal attention, describing their experience as seamless and professional from start to finish.

Advanta IRA continues to lead the self-directed IRA industry through innovation, expertise, and a steadfast commitment to client success, helping investors build wealth on their own terms.

{kind=link}