Real estate has long been a cornerstone of wealth-building strategies. It’s a familiar asset class with tangible value through rental income, appreciation potential, and leverage opportunities.

What many investors don’t realize is that real estate is a popular asset inside retirement accounts by people who use self-directed IRAs (SDIRAs).

For those who want more control over their retirement investments, SDIRAs open the door to a very different approach to long-term investing.

What Is a Self-Directed IRA?

A self-directed IRA is an IRA that allows for a broader range of investment options beyond traditional stocks, bonds, and mutual funds.

The structure follows the same IRS rules as other IRAs (including contribution limits and distribution requirements). But unlike other IRAs, self-directed IRAs give account holders the ability to invest in alternative assets, including real estate.

That flexibility is what draws many investors to self-direction in the first place.

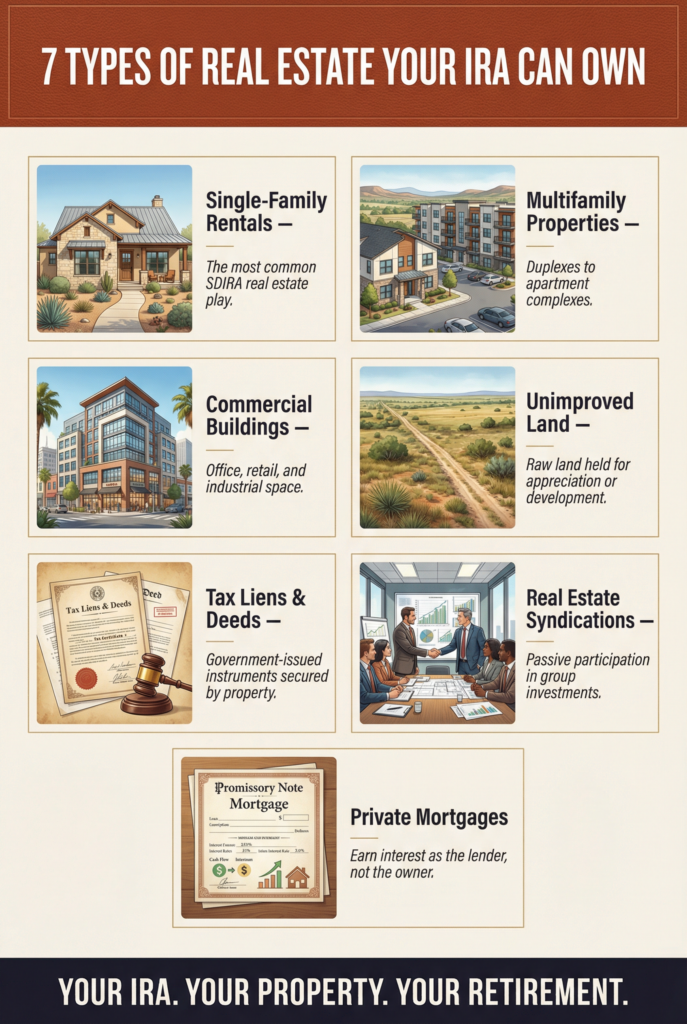

What Types of Real Estate Can Be Held?

A self-directed IRA can hold a wide range of real estate investments, including:

- Single-family rentals

- Multifamily properties

- Commercial buildings

- Unimproved land

- Tax liens and deeds

- Real estate syndications

- Private mortgages secured by property

Some investors choose direct ownership. Others prefer more passive approaches, such as participating in a group investment or private lending arrangement tied to real estate.

The strategy depends on experience level, risk tolerance, and how hands-on an investor wants to be.

How It Works

When purchasing property through a self-directed IRA, the IRA owns the asset.

That means:

- The property is titled in the name of the IRA.

- All income flows into the IRA.

- All expenses are paid from the IRA.

This separation is critical. The IRS prohibits “self-dealing,” meaning the account holder cannot personally benefit from or use the property. For example, you cannot live in the property, vacation there, or rent it to yourself or certain family members or other disqualified persons. These are prohibited transactions that can cause taxation, penalties, and even disqualification of an IRA’s tax-sheltered status.

Income and Growth Potential

One reason real estate fits well inside a retirement account is its potential for both income and appreciation.

Rental income flows into the IRA on a tax-deferred (or tax-free for Roth IRAs) basis. Appreciation also compounds within the account, creating additional capital to reinvest.

Because retirement investing is typically long-term, many investors view real estate as a complementary asset to public market exposure.

That said, it’s not passive by default. Even when property management is outsourced, there are still decisions to be made and compliance rules to follow.

Leverage and Tax Considerations

It’s possible to use financing within a self-directed IRA, but there are specific rules.

If conventional financing is used for an IRA investment, it must be through a non-recourse loan. This means the lender’s only remedy in case of default is the financed property itself, not the individual account holder’s personal assets or other assets in the IRA.

However, unrelated debt-financed income (UDFI) earned by the financed portion may trigger unrelated business income tax (UBIT) within the IRA. This is one of the areas where investors should understand the implications before proceeding and consult the proper tax professionals for guidance.

Real estate inside a retirement account is powerful, but it isn’t a workaround for tax law. It’s a structured strategy that requires awareness and planning.

Direct Ownership vs. Passive Participation

Not every investor wants direct ownership of properties inside their IRA.

Some choose to invest in real estate indirectly through syndications or private funds. In these cases, a sponsor manages the property while investors participate as limited partners.

Others prefer private lending secured by property, earning interest rather than owning equity.

The flexibility of a self-directed IRA allows investors to select the role that aligns with their experience and comfort level.

Is Real Estate in an IRA Right for Everyone?

Real estate in a self-directed IRA isn’t inherently better than traditional investing. It’s simply different.

It requires:

- Comfort with alternative assets

- Understanding of compliance rules

- Willingness to conduct research and due diligence

- A long-term mindset

For investors who want broader control over their retirement strategy, it can be an effective way to diversify beyond public markets.

For others, traditional brokerage accounts may be sufficient.

Closing Thoughts on Real Estate Investing in a Self-Directed IRA

At its core, real estate investing in an IRA is about optionality.

This strategy allows retirement investors to align long-term capital with tangible assets, structured income opportunities, or group investments, all within a tax-advantaged framework.

As with any strategy, clarity comes first. Understanding the rules, the risks, and the structure ensures that real estate becomes a thoughtful component of a retirement plan and not just an interesting idea. Partnering with a self-directed IRA administrator or custodian familiar with real estate transactions is also key.

Because self-direction isn’t about chasing what’s popular.

It’s about building a strategy that supports the retirement life you desire.

{kind=link}