This Content Is Only For Subscribers

If you read our recent feature, Landlord Legal Lowdown: Understanding Depreciation Rules for Texas Rentals, you already know that depreciation is one of the most powerful—but often misunderstood—tax tools landlords have. Still, the word “depreciation” tends to make eyes glaze over. So let’s break it down into basics every landlord should know, whether you own one rental home in Dallas or a small portfolio across Texas.

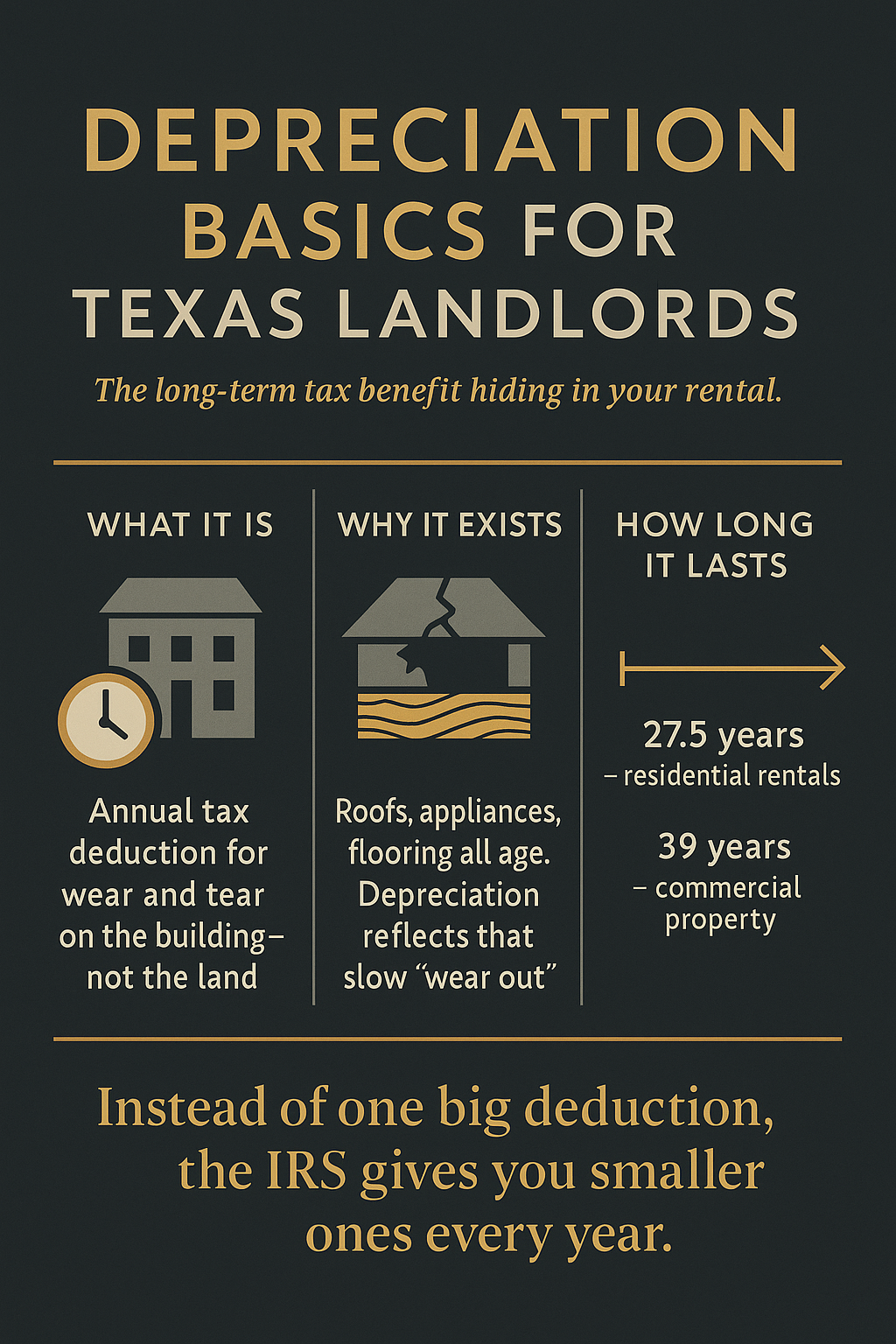

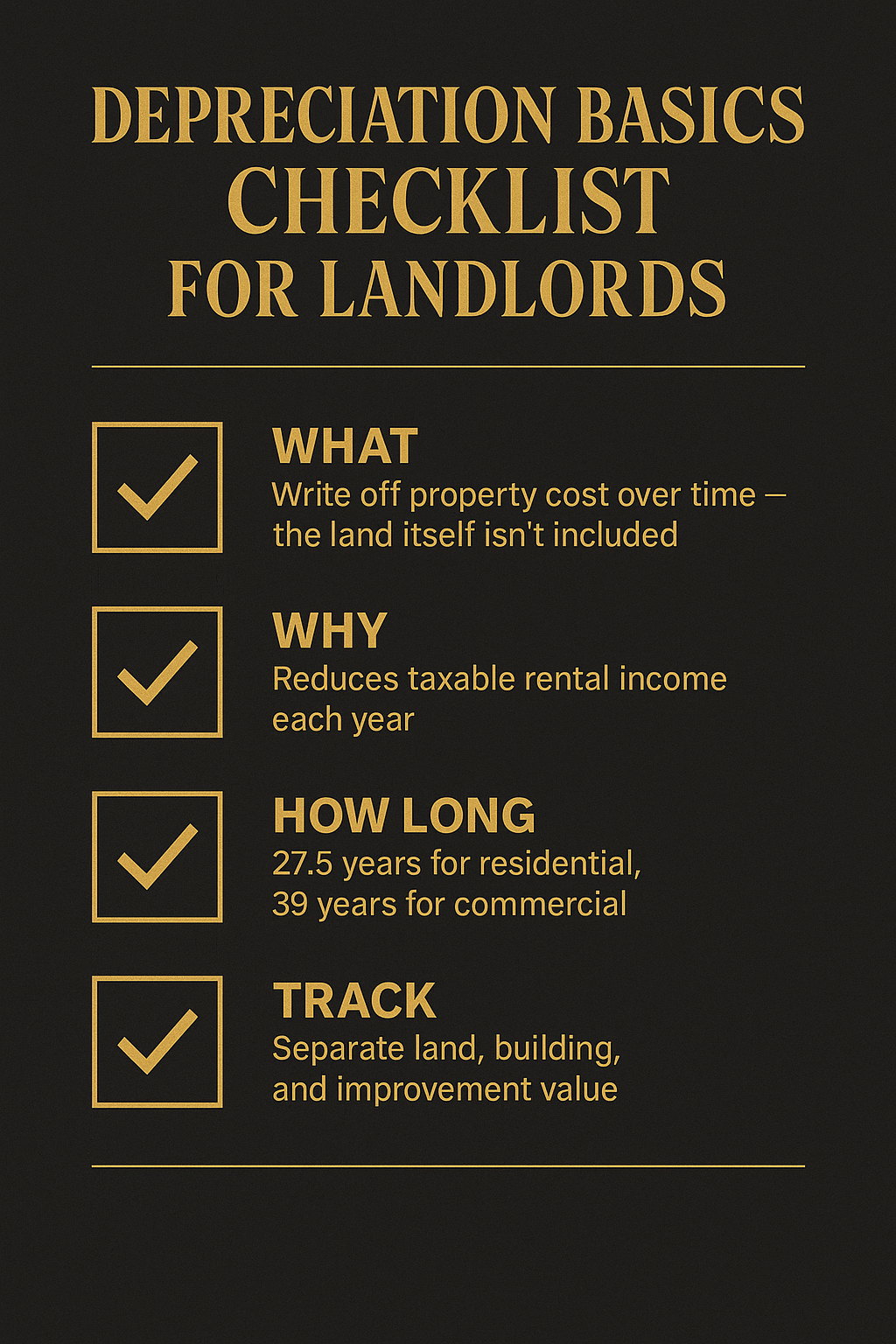

What Is Depreciation, Really?

Think of depreciation as the IRS’s way of recognizing that your rental property wears out over time. While you may see your property’s market value rise thanks to Texas’s strong real estate market, the IRS focuses on the physical structure itself—walls, roof, appliances, flooring. Those things eventually need repair or replacement.

Instead of writing off the cost of your property all at once, the IRS lets you deduct a portion of its value each year over a set number of years. For residential rental properties, that’s 27.5 years. For commercial properties, it’s 39 years.

How It Works in Practice

Let’s say you buy a single-family rental for $300,000. You can’t depreciate the entire purchase price, though. The value of the land is excluded since land doesn’t “wear out.” If the land is worth $60,000, that leaves $240,000 for the building itself.

Divide that $240,000 by 27.5, and you get roughly $8,727 per year in depreciation. That’s a tax deduction you can take annually—before considering repairs, management fees, or other expenses.

Improvements vs. Repairs

One of the biggest points of confusion is knowing what counts as a repair versus what has to be depreciated as an improvement.

- Repairs: Fixing a leaky faucet, patching a hole in drywall, or replacing a broken window. These are usually deductible right away.

- Improvements: Installing a new roof, upgrading the HVAC system, or remodeling a kitchen. These add long-term value, so the IRS requires you to spread the deduction out through depreciation.

Getting this wrong is one of the most common landlord mistakes, and it’s one reason many turn to CPAs familiar with real estate.

Why Depreciation Matters

Depreciation can significantly lower your taxable rental income, even when your cash flow looks strong. In fact, some landlords find they’re able to show little or no taxable income because depreciation offsets so much of their earnings. That means more money stays in your pocket each year.

But remember: depreciation isn’t optional. The IRS expects you to claim it. And when you sell, you’ll likely face something called “depreciation recapture,” where the IRS collects taxes on the deductions you’ve taken. (We cover that more in our longer feature.)

The Bottom Line

Depreciation may sound like dry tax code, but for landlords, it’s a game-changer. It rewards you for the reality that buildings wear down, and it can give you thousands in deductions year after year.

So, as we stressed in Understanding Depreciation Rules for Texas Rentals, don’t overlook it. Track your property’s basis carefully, separate land from building value, and when in doubt, consult a tax professional who understands real estate.

Your bottom line will thank you—both at tax time and when planning your long-term rental strategy.

{kind=link}