This Content Is Only For Subscribers

Tax season can feel overwhelming for Texas landlords. Between gathering receipts, tracking rental income, and categorizing expenses, it’s easy for important details to slip through the cracks. Professional property managers, however, make this process much simpler, helping landlords keep clean, organized books that are ready for the CPA and compliant with IRS guidelines.

Why Good Books Matter

Accurate records are more than a tax-time convenience—they’re protection. Clear documentation supports the numbers on your return if you’re ever questioned and gives you a picture of how well your rentals are performing. Well-kept books can show whether a property is truly cash-flow positive and how much you’re spending on maintenance. A good property manager builds this discipline into your operations so you’re not scrambling every spring.

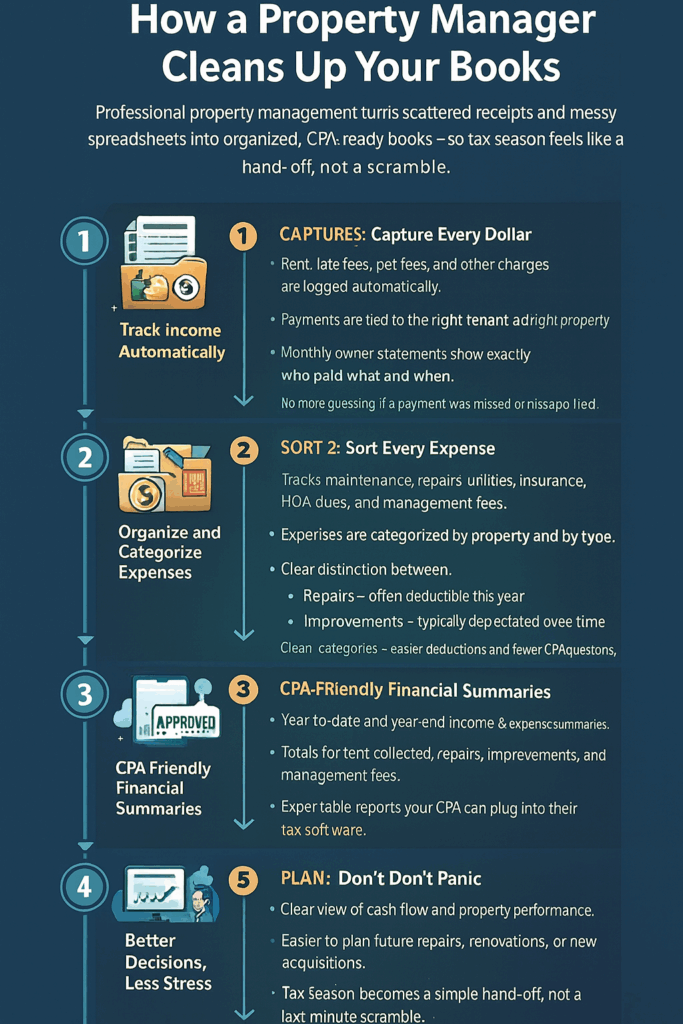

Tracking Income Automatically

One of the most valuable ways property managers help is by tracking income. Rent payments, late fees, and incidental charges like parking, storage, or pet fees are recorded and categorized automatically in modern property management software. Landlords can see who paid what, when, and for which property, eliminating the guesswork that comes with manual spreadsheets.

Most managers reconcile deposits to your bank account, so every dollar that hits your account is matched to a tenant and a property. Monthly owner statements or summaries are usually available online, giving you a clear snapshot of financial activity and simplifying tax preparation for both you and your CPA.

Organizing and Categorizing Expenses

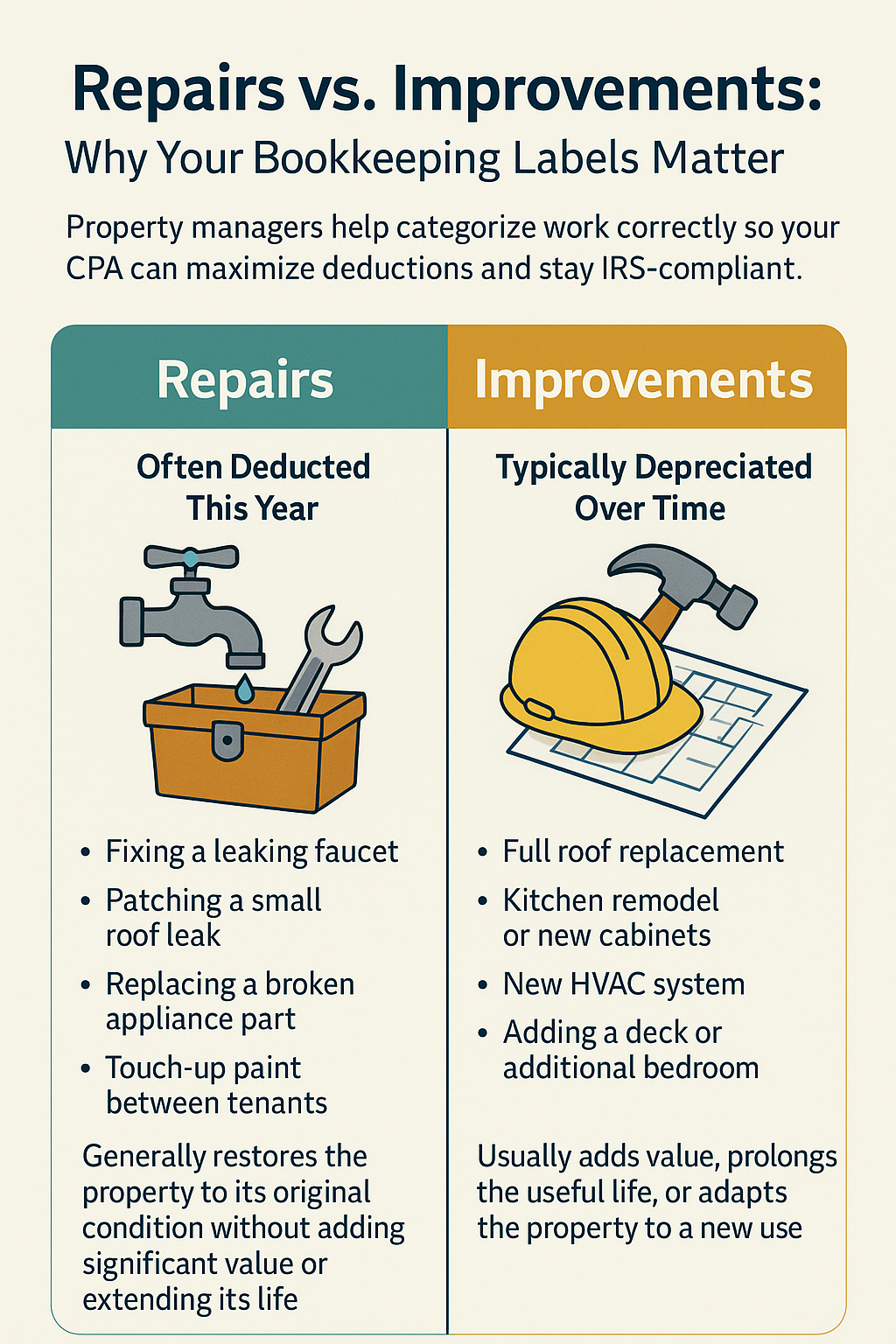

Property managers also track expenses, from routine maintenance and emergency repairs to utilities, insurance premiums, HOA dues, and management fees. Proper categorization is crucial—especially when distinguishing between repairs (which can often be deducted immediately) and improvements (which may need to be depreciated over time).

For example, fixing a leaky faucet is usually a repair, while replacing kitchen cabinets is likely an improvement. When these items are coded correctly from day one, your CPA doesn’t have to guess, and you’re less likely to miss deductions or misclassify major projects. Good expense tracking also makes it easier to separate property-related costs from personal spending.

Documenting Receipts and Invoices

Physical paperwork can get lost, especially for landlords managing multiple properties or juggling a full-time job. Property managers often use digital platforms to store receipts and invoices, linking them directly to the associated expense or property. A plumbing invoice, for instance, can be uploaded, tagged to the correct unit, and stored with the date, vendor, and work description.

This creates an organized, searchable audit trail that CPAs can review without digging through shoeboxes of paper. If the CPA has a question about a large repair or an unusual charge, your manager can usually pull up the supporting document in seconds.

Generating CPA-Friendly Reports

Many property managers provide financial summaries specifically designed for tax preparation. These reports may include total rent collected, security deposit activity, deductible repair costs, management fees, and other key financial metrics. Some can even export directly into common accounting or tax software formats.

With this information already organized, CPAs can focus on tax strategy—like how to handle depreciation or passive losses—rather than compiling basic data. That saves professional fees, reduces stress for landlords, and lowers the risk of errors on your return.

Reducing Stress and Improving Planning

A well-organized set of books doesn’t just help at tax time; it helps landlords make smarter decisions about their portfolio year-round. Accurate financial records allow property owners to monitor cash flow, compare performance between properties, and plan for big-ticket items like roofs or major renovations.

When you can see your numbers clearly, you’re better equipped to decide whether to raise rents, refinance, sell, or acquire another property. Professional bookkeeping through a property manager adds credibility when sharing reports with lenders or partners.

The Bottom Line

Professional property management isn’t just about maintenance calls or tenant communications—it’s about keeping your financial records precise, accessible, and CPA-ready. For Texas landlords, partnering with a property manager means smoother tax preparation, maximized deductions, and fewer surprises when it’s time to sign your return. Instead of scrambling every spring, you can hand your CPA an organized financial picture and focus on what matters most: growing and protecting your investment portfolio year-round.

{kind=link}