This Content Is Only For Subscribers

For most landlords, tax season is about as welcome as a midnight call from a tenant about a burst water pipe. Between balancing income, sorting receipts for repairs, and trying to remember if that new roof counts as a deduction or a depreciation item, the paperwork can feel endless.

This is exactly where professional property managers prove their worth. Beyond handling tenant calls, collecting rent, and coordinating repairs, property management companies are quietly keeping track of the very records that make your tax return accurate—and less stressful.

In this article, we’ll walk through exactly how property managers help simplify tax season. From documenting income streams to tracking deductible expenses, generating year-end reports, and offering landlord-specific insights, management services can give landlords confidence that nothing important slips through the cracks.

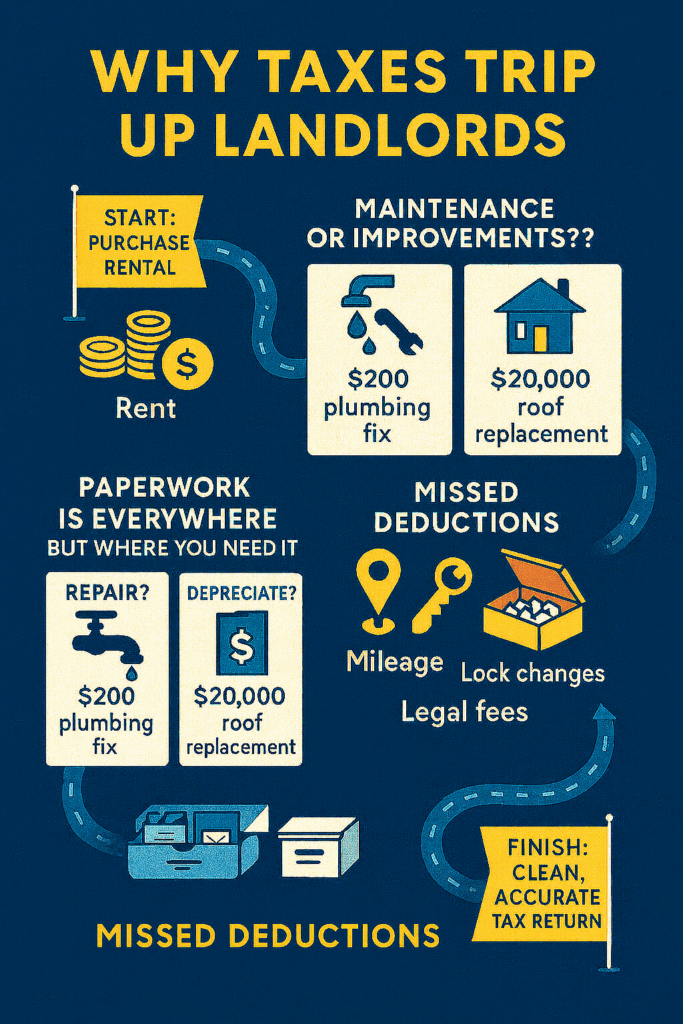

Why Taxes Trip Up Landlords

Even experienced landlords will admit that the financial side of property management can get messy. The most common challenges include:

- Multiple income streams: Rent payments, late fees, pet fees, storage unit rentals, parking fees, and even laundry machines all generate income that needs to be reported. Missing just one of these streams can skew your return.

- Maintenance tracking: A $200 plumbing repair is simple enough, but what about a $20,000 roof replacement? Is it deductible in one year or must it be depreciated? Many landlords guess, which can cause IRS trouble later.

- Mixed records: If you’ve ever had receipts scattered in glove boxes, email inboxes, or in a shoebox under your desk, you know how quickly disorganization spirals.

- Unclear deductions: Landlords often overlook valid deductions, like mileage to the property, lock changes, or even certain legal fees.

Taxes for rental property owners aren’t impossible, but they require attention to detail and consistent record-keeping. The good news? A property manager’s systems are designed to handle exactly that.

Rent Collection and Income Tracking

The first and most obvious way property managers help at tax time is by tracking income automatically.

Most management companies use professional software platforms that log every transaction the moment it happens. This includes:

- Monthly rent

- Late fees

- Pet deposits or pet rent

- Application fees

- Parking or storage rentals

- Utility reimbursements

- Miscellaneous tenant charges

Each payment is timestamped, categorized, and linked to the tenant’s account. That means when April rolls around, landlords don’t have to scroll through bank statements with a highlighter, trying to figure out what was rent and what was a security deposit refund.

At year-end, property managers generate a detailed income report. This not only makes filling out Schedule E of your tax return much simpler, but it also provides supporting documentation in case of an IRS inquiry.

For landlords with multiple properties, the value here multiplies. Instead of juggling spreadsheets for each address, a single consolidated report provides a clean snapshot of annual rental income.

Expense Tracking and Deduction Management

If rent collection is the “income” side of the equation, expense tracking is the “deduction” side—and it’s where many landlords leave money on the table.

Property managers are already paying invoices and coordinating maintenance throughout the year. Every plumber visit, landscaping contract, HVAC repair, and roof replacement gets logged. Because management systems categorize expenses automatically, you get a year-end breakdown that separates repairs, maintenance, improvements, and capital expenses.

This distinction matters. For example:

- Repairs and maintenance (like fixing a leaky sink or replacing a broken window) can usually be deducted immediately.

- Capital improvements (like new flooring, a new HVAC system, or a kitchen remodel) typically have to be depreciated over several years.

Rather than scrambling to reconstruct your expenses from a year’s worth of receipts, property managers hand you a ready-to-go report showing exactly what was spent and where it fits on your return.

They also ensure you don’t forget smaller deductible items, such as:

- Lock and key replacements

- Pest control services

- Property management fees (yes, their own services are deductible!)

- Professional fees (lawyers, accountants, appraisers)

- Mileage or vendor trip charges

Landlords who self-manage often miss these smaller items simply because they aren’t tracked consistently. Over time, that can mean hundreds or thousands of dollars in unclaimed deductions.

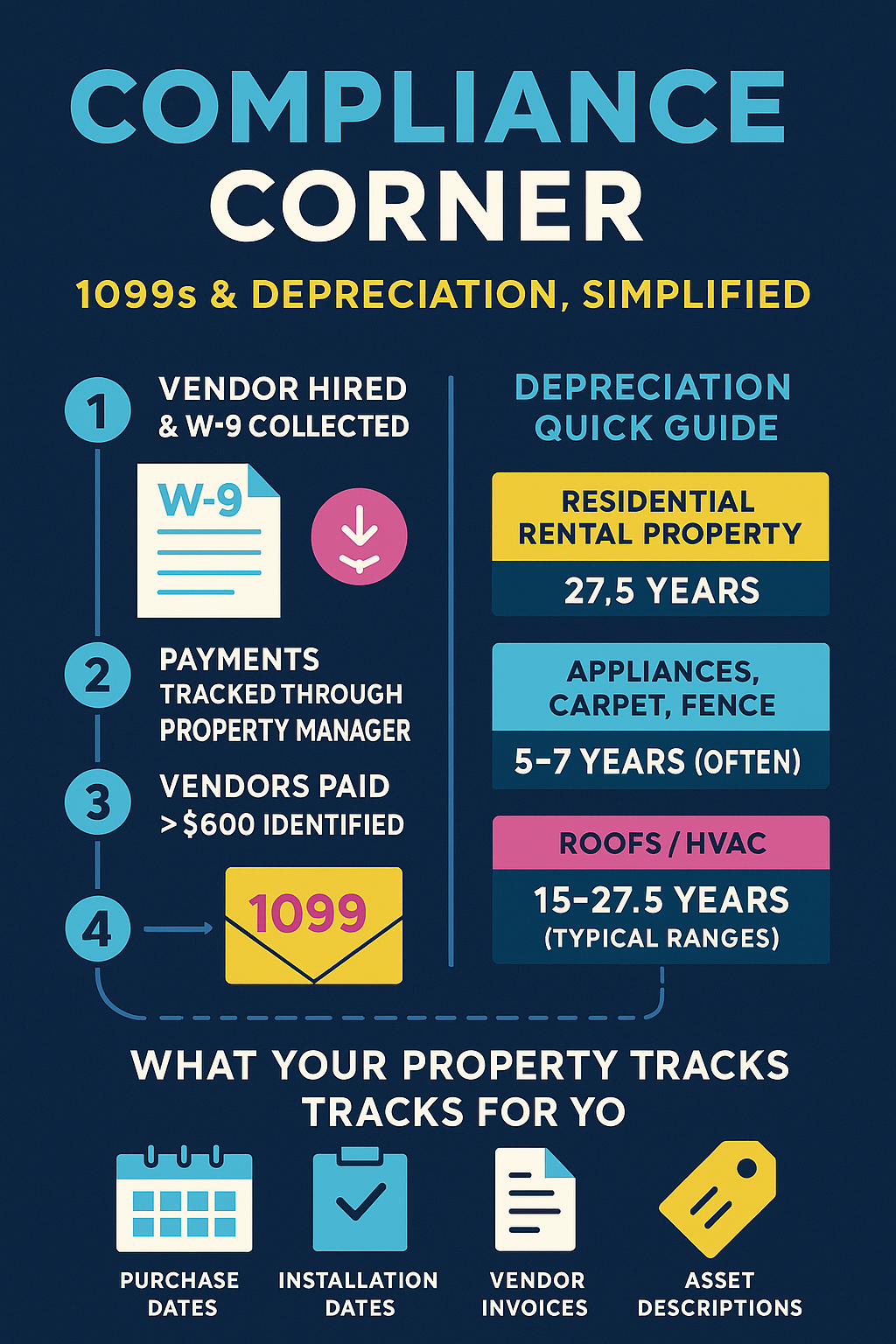

1099 Forms and Vendor Records

Another tax-time headache for landlords is issuing 1099-NEC forms to vendors and contractors paid more than $600 in a calendar year.

Property managers take care of this automatically. Since they already collect W-9s and track payments to vendors, they can issue 1099s on your behalf or provide you with the records needed to complete them.

This ensures you remain compliant with IRS requirements while avoiding the scramble of trying to remember how much you paid that landscaping crew or electrician last spring.

Depreciation Guidance and Documentation

While property managers aren’t tax advisors, they can provide the documentation your CPA needs to calculate depreciation correctly.

Depreciation allows landlords to deduct the cost of the building and certain improvements over time. For example:

- Residential rental property: depreciated over 27.5 years

- Appliances, carpeting, or fences: often depreciated over 5–7 years

- Roofs or HVAC systems: typically depreciated over 15–27.5 years

Since property managers track exactly when assets are purchased and installed, they provide the timeline your accountant needs to file accurately. That means fewer guesses, fewer missed deductions, and fewer red flags in the event of an audit.

Handling Security Deposits Properly

Security deposits can be another gray area at tax time. If you keep part of a tenant’s deposit to cover damages, that portion becomes taxable income. If you refund it, it does not.

Because property managers document deposits carefully—recording the initial payment, deductions for damages, and any refund—they provide a clear record of what is and isn’t income. This prevents landlords from accidentally misreporting deposits, which is a common audit trigger.

Consolidated Year-End Reports

The single most valuable deliverable property managers provide at tax time is the consolidated year-end report.

This report typically includes:

- Total rental income per property

- Total expenses, broken down by category

- Net operating income

- Copies of invoices and receipts (if requested)

- Vendor payment records for 1099s

- Security deposit ledgers

For landlords juggling multiple properties, this kind of organized, professional reporting is the difference between a smooth tax appointment and a stressful, paper-scattered nightmare.

Peace of Mind During an Audit

No landlord wants to face an IRS audit—but it happens. And when it does, having organized records is half the battle.

Property managers don’t just provide neat summaries; they provide supporting documentation—receipts, invoices, contracts, and logs. That means if the IRS questions a $4,000 roof charge, you can point to the exact invoice, date of service, and contractor information.

This level of record-keeping doesn’t just protect you; it shortens the audit process dramatically.

Beyond Taxes: The Hidden Benefits of Manager-Led Bookkeeping

The benefits of professional bookkeeping go beyond April 15. Throughout the year, landlords gain insights from the same systems used for tax reporting:

- Cash flow tracking: Are certain properties consistently underperforming?

- Budget planning: How much are you really spending on maintenance annually?

- Rent growth analysis: Do your rent increases cover rising expenses?

This data helps landlords make better long-term decisions, not just file accurate tax returns.

Technology is Changing the Game

The tools property managers use today are far more advanced than the spreadsheets of the past. Modern property management software integrates with accounting systems, automates recurring payments, and even provides owner portals where landlords can download real-time financial reports.

For landlords who value convenience, this means tax prep isn’t just easier at year-end—it’s a transparent process all year long. You can log in anytime, see updated numbers, and even export reports directly for your CPA.

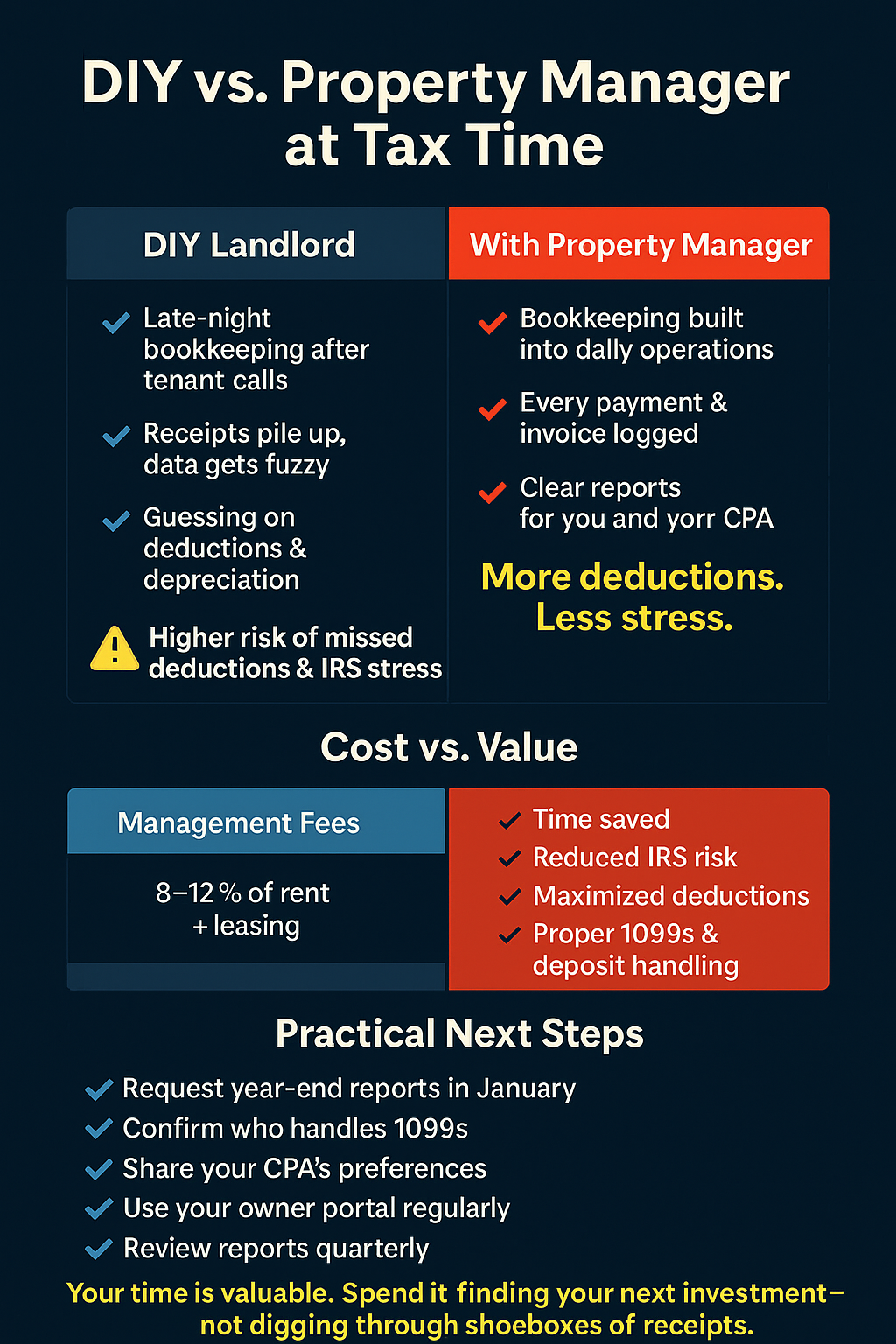

Why DIY Landlords Still Struggle

Some landlords argue they can track everything themselves. And yes, with discipline, a self-managed landlord can keep clean books. But many underestimate the time commitment.

Between tenant calls, leasing, and handling repairs, bookkeeping often gets pushed aside. Receipts pile up. Bank statements blur together. By the time tax season arrives, reconstruction is nearly impossible.

Property managers eliminate this problem by building bookkeeping into the daily rhythm of property operations. Every rent payment, vendor bill, and deposit is recorded in real time—not months later.

The Cost vs. Value of Property Management at Tax Time

Of course, property management isn’t free. Typical fees range from 8–12% of monthly rent, plus leasing fees. But when evaluating cost, landlords should factor in:

- Time saved during tax season

- Reduced stress and fewer IRS risks

- Maximized deductions through accurate tracking

- Professional compliance with 1099s and deposit laws

In many cases, the extra deductions identified and claimed thanks to proper bookkeeping can offset part of the management fee itself.

Practical Tips for Landlords Using Property Managers

If you already work with a property manager, here are a few ways to maximize their help at tax time:

- Request year-end reports early. Don’t wait until April—ask for them in January.

- Ask about 1099 handling. Clarify whether your manager issues them or provides vendor totals for your CPA.

- Share your CPA’s needs. Some accountants prefer digital files, others want paper. Let your manager know upfront.

- Use the owner portal. Many landlords underutilize these systems. Explore the reports available in real time.

- Review reports quarterly. Don’t wait until year-end to spot trends or errors.

Final Thoughts

Tax season will never be exciting, but it doesn’t have to be overwhelming. Property managers are more than just rent collectors—they’re your partners in keeping financial records clean, accurate, and audit-proof.

From logging every rent payment to categorizing repairs, issuing 1099s, and preparing year-end reports, professional management turns tax prep from a dreaded chore into a straightforward process.

For landlords juggling multiple properties—or even just one busy rental—partnering with a property manager may be the smartest tax decision you can make.

Because at the end of the day, your time is valuable. And wouldn’t you rather spend it finding your next investment, rather than digging through shoeboxes of receipts?

{kind=link}