If you’re exploring a self-directed IRA (SDIRA), you’ve likely come across two terms: custodian and administrator. They’re often used interchangeably, which can make the terms confusing.

Understanding the distinction and why it matters is an important step in choosing the right partner for your retirement account.

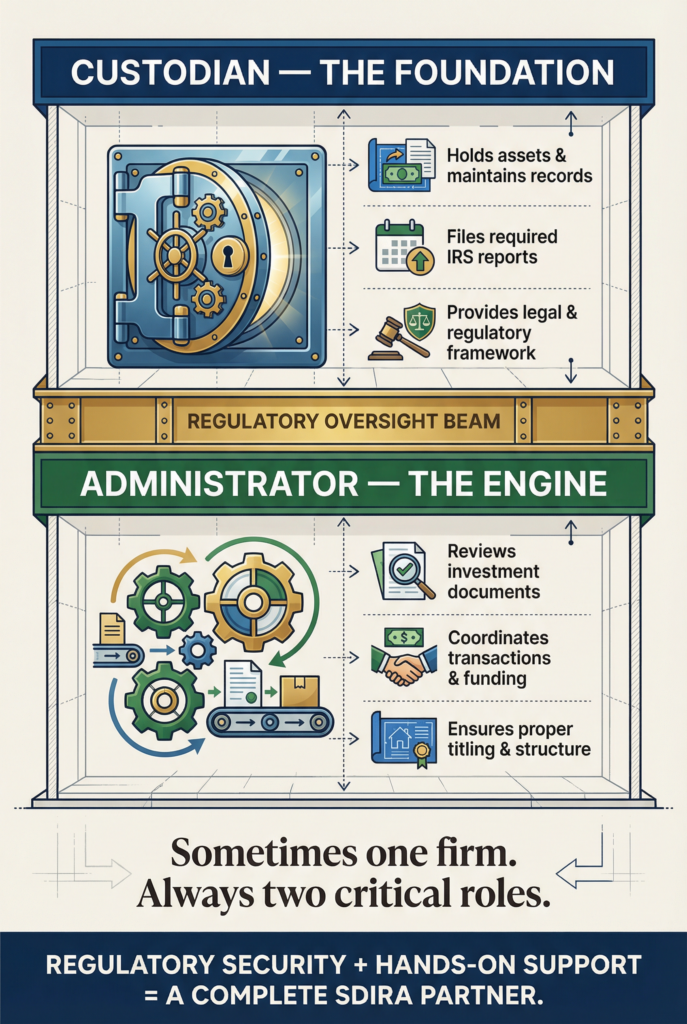

What Is a Custodian?

A custodian is a financial institution responsible for holding retirement account assets and ensuring the account complies with IRS regulations. By law, IRAs must be held by a qualified custodian. The custodian maintains records, files required IRS reports, and safeguards the assets held within the account.

In traditional brokerage IRAs, the custodian typically limits investments to stocks, bonds, mutual funds, and other publicly traded assets. In the self-directed space, however, custodians support alternative investments such as real estate, private lending, private equity, precious metals, and more.

The key point: a custodian provides the legal framework and regulatory oversight required for an IRA to exist.

What Is an Administrator?

An administrator focuses on the operational side of the account.

While custodians hold the assets and handle reporting, administrators often manage the day-to-day processes. This includes reviewing investment documents, coordinating transactions, facilitating funding, and ensuring that investments are properly titled and structured.

Sometimes, the custodian and administrator roles are housed under the same umbrella. Others operate separately but work together. Either way, investors primarily interact with the administrator during the investing process.

Custodians provide the regulatory backbone; administrators provide the hands-on support.

Why the Difference Matters

Not all self-directed IRA providers operate the same way.

Some firms limit the types of investments they process. Others specialize in only one or two asset classes. And some rely heavily on automation, offering portals and digital tools with minimal human interaction.

For some investors, that may be enough. For others, responsive, knowledgeable support matters.

Self-directed investing isn’t structured in the same way traditional brokerage investing is. It involves contracts, operating agreements, subscription documents, wire instructions, and compliance considerations that account owners must understand. Having an experienced team to help review documentation and guide the process can make a significant difference.

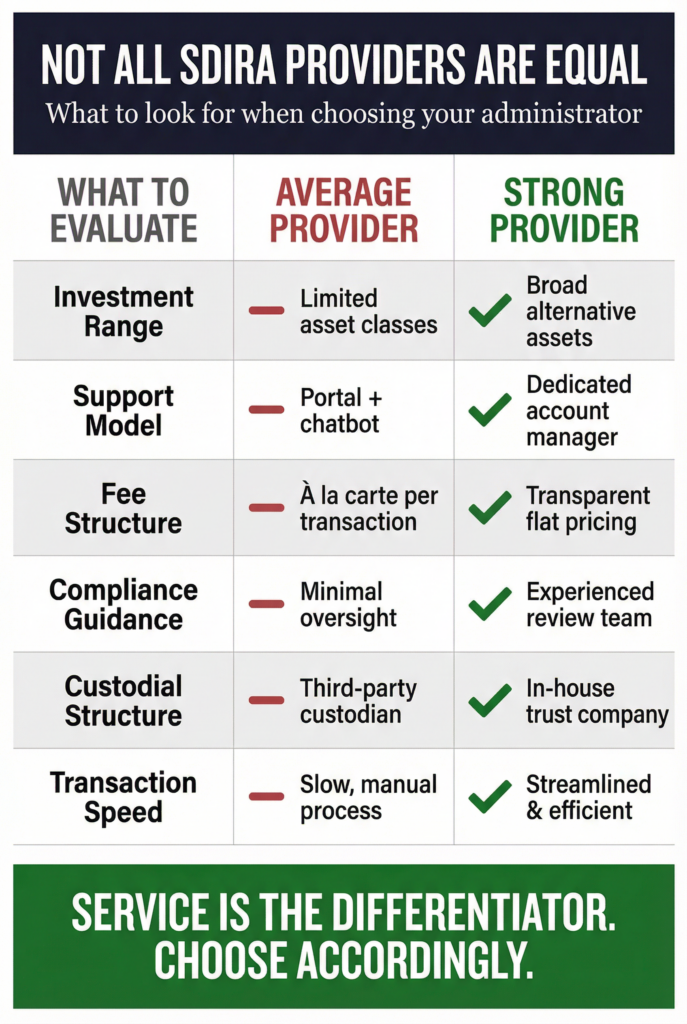

Not All SDIRA Administrators Are Equal

The level of operational clarity and support self-directed IRA companies provide can differ substantially. None sell investments, but some administrators limit certain investments, while others allow every alternative asset available. Some charge à la carte fees that increase with every transaction. Others provide limited guidance on compliance considerations such as prohibited transactions or disqualified persons.

This is where service becomes a differentiator.

The Advanta IRA Difference

In a world increasingly built around automation and chatbots, many investors still prefer working with real people, especially when their retirement savings are involved.

Advanta IRA combines the required custodial structure with high-touch administrative support. Every client works with a dedicated account manager who understands their account history, investment strategy, and long-term goals. Instead of navigating a generic call center, investors have a direct point of contact.

Advanta IRA also supports a broad range of alternative investments. From private lending and private equity to precious metals, real estate, venture capital, and more, the firm is structured to accommodate diverse asset classes rather than funnel investors into a narrow lane.

That flexibility matters. Retirement strategies evolve over time, and investors shouldn’t feel constrained by administrative limitations.

Equally important is compliance support. While no administrator can provide legal or tax advice, experienced teams can help ensure transactions are processed correctly and structured in alignment with IRS guidelines.

To further strengthen its structure and provide long-term continuity for clients, Advanta IRA formed Advanta Trust Company, a Nevada-chartered trust company that now serves as custodian for client assets. This move brings custodial oversight in-house under the Advanta umbrella, enhancing stability, regulatory clarity, and operational alignment. For investors, it means their accounts are supported by a cohesive team with shared standards, streamlined processes, and a long-term commitment to safeguarding retirement assets. It’s another step toward delivering both flexibility in alternative investing and confidence in the custodial framework behind it.

Choosing the Right Partner

When evaluating custodians and administrators for a self-directed IRA, consider more than just fees.

Ask:

- What types of investments are permitted?

- How accessible is the support team?

- Will I have a dedicated point of contact?

- How experienced is the firm in processing complex alternative transactions?

A self-directed IRA is a powerful vehicle. But its performance depends on the structure and support behind it.

The right custodian and/or administrator should provide both regulatory security and practical clarity giving you the confidence to focus on investment strategy rather than paperwork.

Because self-direction isn’t just about having more investment options. It’s about having the right team in your corner every step of the way.

{kind=link}