This Content Is Only For Subscribers

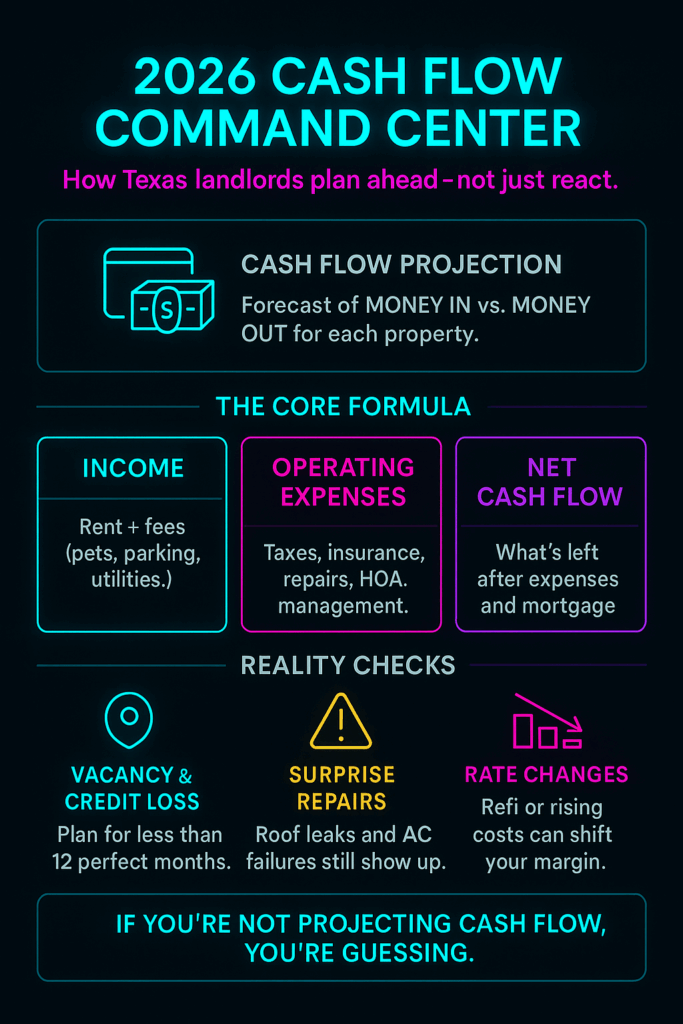

As 2026 approaches, Texas landlords are looking ahead to make smart investment decisions, not just react to headlines. One of the most powerful tools for planning is a simple but disciplined cash flow projection. By estimating income and expenses for the coming year, landlords can spot potential profits, prepare for challenges, and make informed choices about buying, selling, or holding rental properties.

At its core, a cash flow projection is a forecast of money moving in and out of each property. It starts with gross rental income: scheduled monthly rent, pet fees, parking, or utility reimbursements. From there, owners subtract anticipated operating expenses to see what is left over each month and each year. Mortgage payments, property taxes, insurance, HOA dues, repairs, maintenance, utilities, and management fees all need to be included. A realistic projection also builds in a vacancy and credit-loss factor so you are not counting on 12 perfect months of rent.

For example, a landlord might assume a 5–8% vacancy allowance for a single-family home in the suburbs and a slightly higher allowance for a small apartment building in a more transient neighborhood. Even if every unit is currently occupied, planning for turnover keeps your forecast honest and your reserves prepared.

To illustrate how this works in practice, imagine three sample Texas rentals you own in 2026: a Houston single-family home, a Dallas–Fort Worth duplex, and a San Antonio townhouse. After subtracting all expenses, the Houston property might generate $800 per month, the DFW duplex could yield $1,400, and the San Antonio unit might bring in $550. Seeing those numbers side by side makes it easier to decide where to focus renovations, which loan to pay down fastest, or which market might be best for your next purchase.

Cash flow projections aren’t just spreadsheets for your files—they should drive day-to-day decisions. If a property is projected to have tight margins, you may choose to schedule preventive maintenance now to avoid a big emergency repair later. You might test a small rent increase at renewal, add a utility reimbursement, or explore refinancing to lower your monthly payment. On the other hand, a property with strong projected cash flow can support more ambitious moves, such as adding a second unit over a garage, converting a long-term rental to a higher-yield mid-term strategy, or using the surplus to fund the down payment on another home.

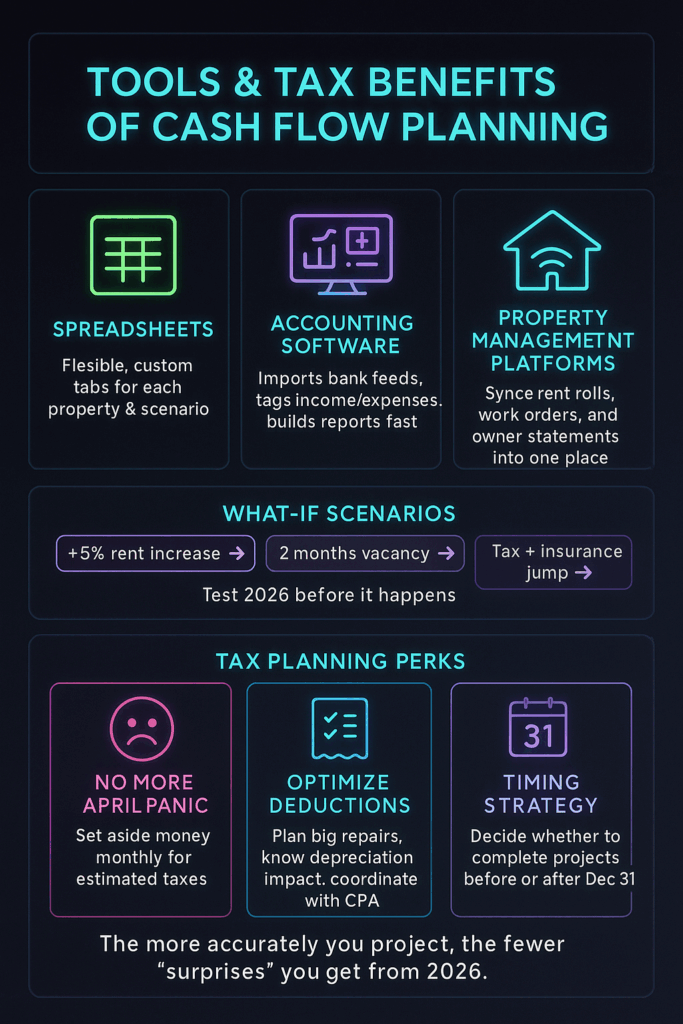

Technology can make this process far less intimidating. Many landlords still use spreadsheets, which work well as long as the assumptions are updated regularly. Others rely on bookkeeping tools like QuickBooks or dedicated property-management software that pulls in actual income and expenses from bank feeds. With a few clicks, you can copy last year’s numbers, tweak expected rent, taxes, or insurance for 2026, and instantly see how those changes affect your bottom line. Building a few “what-if” scenarios—optimistic, conservative, and worst-case—helps you understand how sensitive your portfolio is to vacancies, rate hikes, or big repairs.

Cash flow projections are just as important for tax planning. Knowing your estimated income and expenses in advance lets you set aside money each month for income taxes instead of scrambling in April. It also highlights opportunities to accelerate or defer certain expenses. For instance, if 2026 looks like a high-income year, you may decide to complete larger repairs before December 31 so you can deduct them sooner. Projections also keep depreciation schedules and loan interest top of mind, making conversations with your CPA more strategic and less rushed.

Ultimately, the goal of projecting cash flow is not to predict the future perfectly—no spreadsheet can do that—but to give yourself a roadmap. For Texas landlords, 2026 will likely bring continued demand, evolving costs, and new opportunities. By regularly updating your projections and using them to guide decisions about rent levels, reserves, and acquisitions, you gain something every investor wants: clarity and confidence.

Whether you are evaluating a new purchase, deciding if it is time to sell an underperforming property, or simply preparing for tax season, cash flow projections turn scattered numbers into a clear story about your portfolio. The more clearly you can see that story, the easier it becomes to choose your next move in 2026 and beyond.

{kind=link}