This Content Is Only For Subscribers

In an earlier column, we talked about defining what “success” means for your rental business. Now let’s zoom in on one of the biggest pieces of that success: your income goals for the year.

“Make more money” is not a strategy. As a Texas landlord, you’re dealing with real expenses—taxes, insurance, maintenance, and the occasional surprise from the weather. Your job is to turn that vague desire into clear, realistic targets you can manage toward.

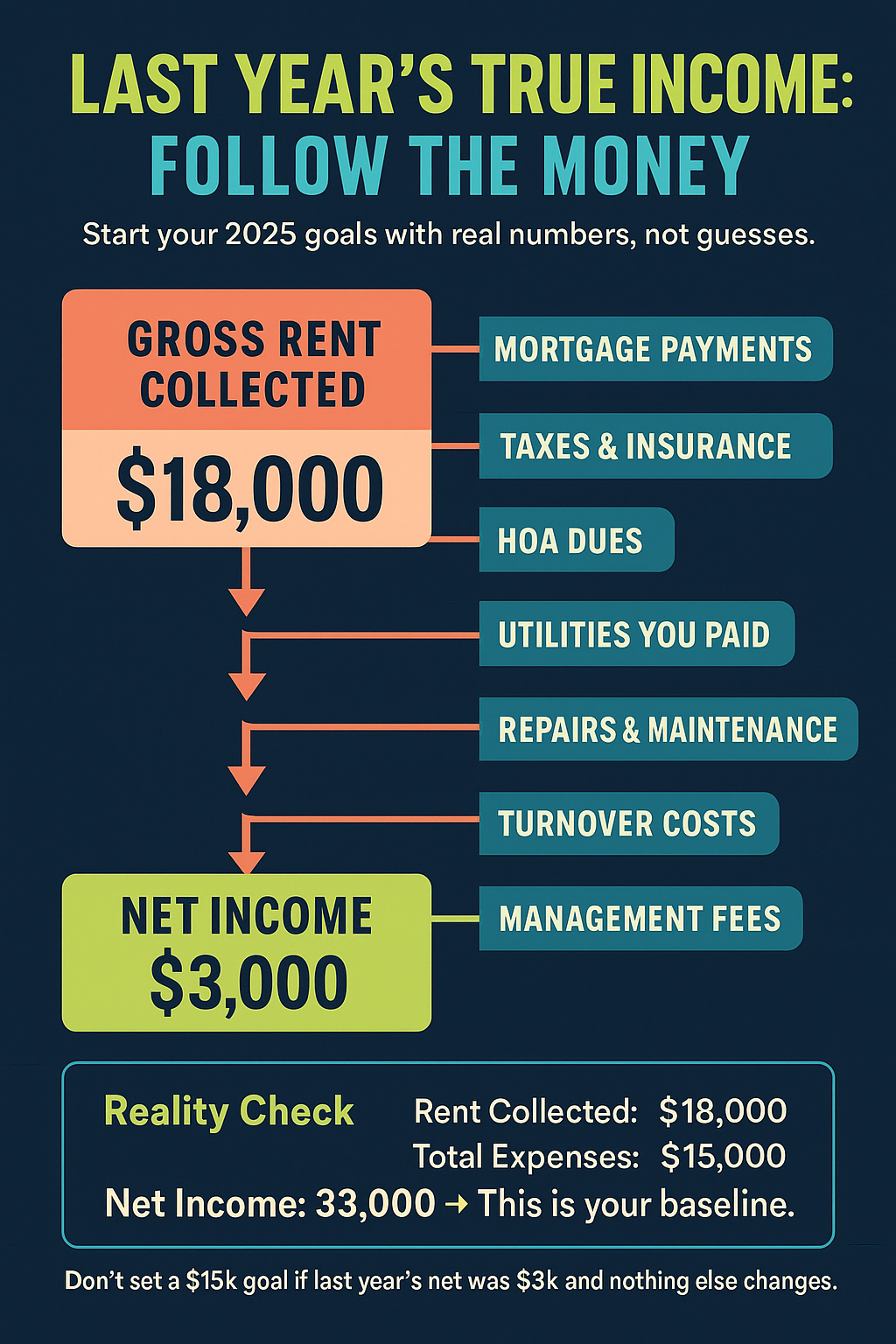

Start with Last Year’s Net (Not Just Rent Collected)

Before you set new goals, look back at what you actually kept in your pocket.

For each property, total up:

- Rent collected

- Mortgage payments

- Taxes and insurance

- HOA dues (if any)

- Utilities you paid

- Repairs and maintenance

- Turnover costs

- Management fees

Then calculate:

Net income = Rent collected – all expenses

That number is your baseline. If a property netted $3,000 last year, jumping to $15,000 without major changes is fantasy. Aim for a realistic stretch instead of a miracle.

Decide Your Main Focus: Cash Flow or Long-Term Growth

You can’t optimize for everything. For the coming year, which matters more?

- Cash flow now

You want more spendable money each month.- Higher net cash flow per door

- Careful about upgrades that don’t pay off quickly

- Long-term equity and value

You’re okay with modest cash flow in exchange for appreciation and debt paydown.

- More willing to reinvest in improvements

- Thinking in 3–10 year timelines

Example cash-flow goal:

“By year-end, I want an average of $400/month in net cash flow per unit.”

Example long-term goal:

“I want my properties to cover all expenses and reserves while I reinvest any surplus into upgrades.”

Set Per-Property Targets, Not Just a Big Number

Instead of saying, “I want $20,000 this year,” break it down property by property.

For each unit:

- Start with last year’s net income.

- Ask: “What’s a reasonable improvement here?”

Consider:

- Is rent at, below, or above market?

- Can small upgrades justify a higher rent?

- Was vacancy longer than it needed to be?

- Are there recurring expenses you could reduce?

Your total income goal becomes the sum of realistic per-property targets, not a guess.

Don’t Ignore Taxes, Insurance, and Reserves

Texas property taxes and insurance can move more than you’d like. Build that into your plan now.

- Assume some increase in property taxes instead of hoping they stay flat.

- Review insurance at renewal and shop around if it’s been a while.

- Decide what you’ll set aside monthly for:

- Future big-ticket items (roof, HVAC, major appliances)

- Routine repairs

- Vacancy

A solid income goal should be after reserves, not before. For example:

“I want $300/month net per unit after setting aside $100/month in reserves and adjusting for updated taxes and insurance.”

That’s realistic. It acknowledges that things wear out.

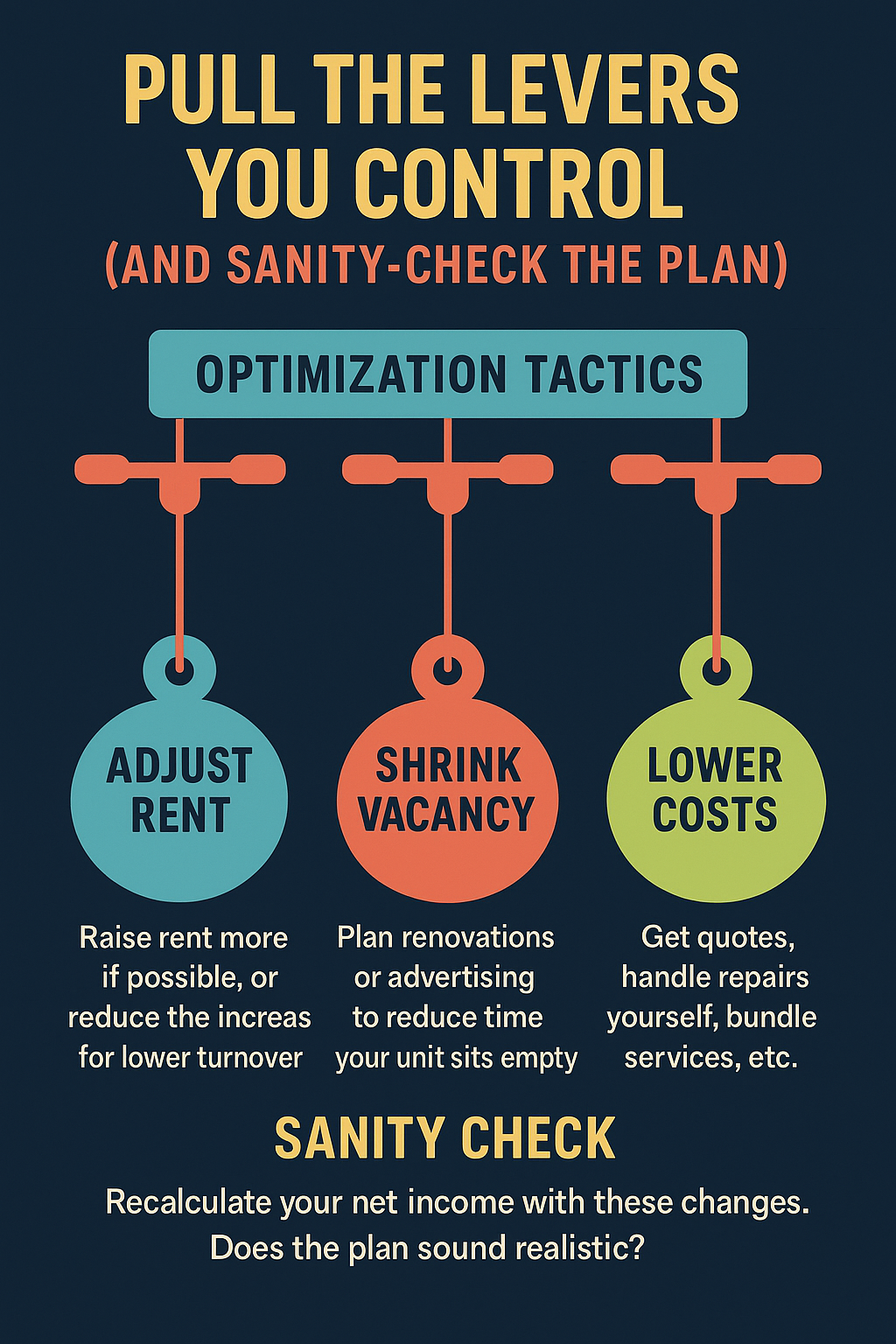

Tie Your Goal to Levers You Actually Control

You don’t control the economy—but you do control some powerful levers:

- Rent – Will you adjust at renewal or for new tenants, and by how much?

- Vacancy – Can you shorten downtime with better marketing and earlier pre-leasing?

- Maintenance strategy – Can you shift from constant “surprise repairs” to basic preventative work?

- Expenses – Can you renegotiate services, shop insurance, or simplify utilities?

Say your goal is:

“Increase annual net income on Property C by $1,500.”

You might get there by:

- A modest rent increase

- Cutting vacancy by a week or two

- Fixing nagging issues now instead of paying for repeat service calls

Now your income target is linked to specific actions, not just optimism.

Sanity-Check Against Your Market and Tenants

Finally, ask:

- Is your target rent in line with comparable units in your part of Texas?

- Are you pairing any increase with value—decent maintenance, small upgrades, responsive communication?

- Does your goal still work if you hit a normal level of vacancy and repairs?

If your plan only pencils out with zero vacancy and zero problems, it’s not a real plan.

Better to set a moderate goal you can meet than a wild one you miss every year.

The Bottom Line

Realistic income goals come from:

- Knowing last year’s true net, not just gross rent

- Choosing whether you’re focused on cash flow or long-term growth

- Setting per-property targets

- Building in taxes, insurance, and reserves

- Connecting goals to levers you can actually pull

Do that, and your rental income for the year stops being a guess—and starts becoming a manageable, trackable result of clear decisions.

{kind=link}