Independent landlords in U.S. cities don’t lose money because they lack hustle, they lose it because rental business finances get treated like an afterthought. The core tension is simple: rent checks come in, expenses drip out, and without financial knowledge it’s hard to tell whether the property is actually performing or quietly draining cash. Landlords who take the numbers seriously get steadier rental property success because decisions stop being guesses and start being measured. Clear records and a real view of performance create leverage for rental income optimization.

Understanding Rental Financial Literacy

Rental financial literacy is the skill of turning rent and receipts into a clear story you can trust. It covers clean bookkeeping, basic accounting rules, what taxes really apply to you, and how to read your key statements. The goal is simple: know your results without guessing.

This matters because “profit” is not your bank balance, and surprises usually show up as late fees, missed deductions, or cash shortages. Understanding a rental property deduction helps you track real profit since you are taxed only on profit, not total rent collected.

Picture a unit that feels fine because the rent clears each month. Then you total repairs, insurance, turnover costs, and taxes and realize the year barely broke even. A simple forecast and one clean set of statements would have shown the squeeze months earlier.

Build a Landlord Money Routine That Runs Weekly

A good routine turns your rentals into a predictable system: you know what you can spend, what you should save, and what needs attention before it becomes a problem. For independent landlords, this is how you protect cash, spot income leaks early, and make growth decisions without guessing.

- 1. Set a “real expenses” monthly budget

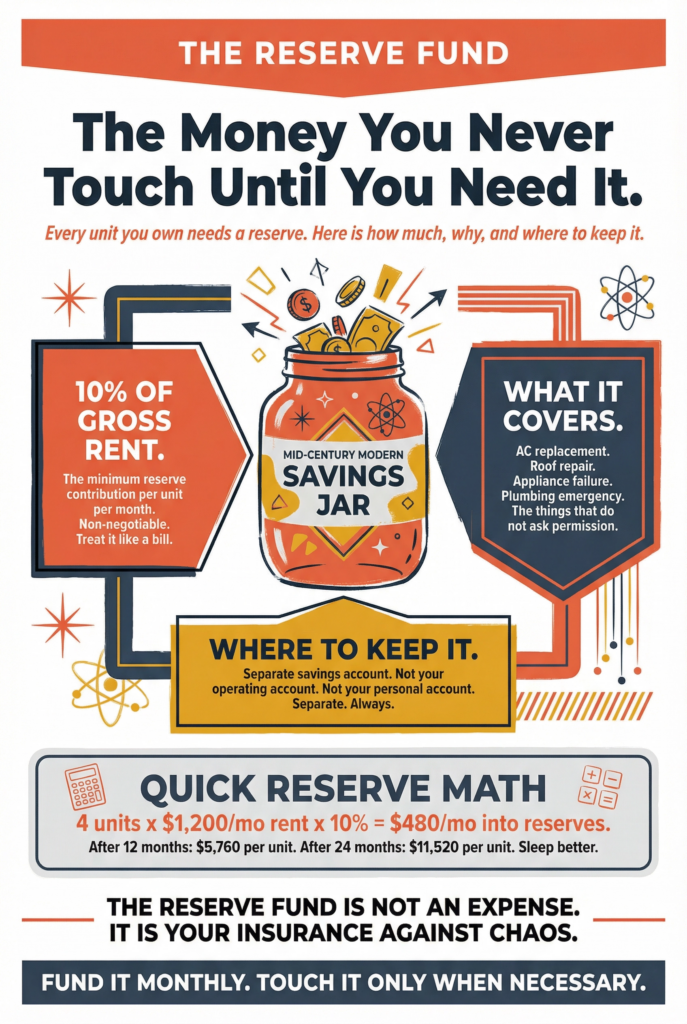

Start with last year’s actual numbers, then build a budget that covers fixed costs, variable repairs, and reserves. Treat cash flow as the gap between rent and day-to-day costs because cash flow is rental income minus operating expenses. Include common line items you might overlook, like property management fees averaging 8.5% of rent if you outsource any part of operations. - 2. Create separate buckets for taxes and reserves

Open separate accounts or labeled “buckets” for taxes, maintenance, and vacancy so the money is there when you need it. Automate transfers on rent day, even if the amount is small, so you do not accidentally spend future obligations. This single move reduces the odds of late payments, rushed repairs, or credit card float. - 3. Do a 15-minute weekly cash check-in

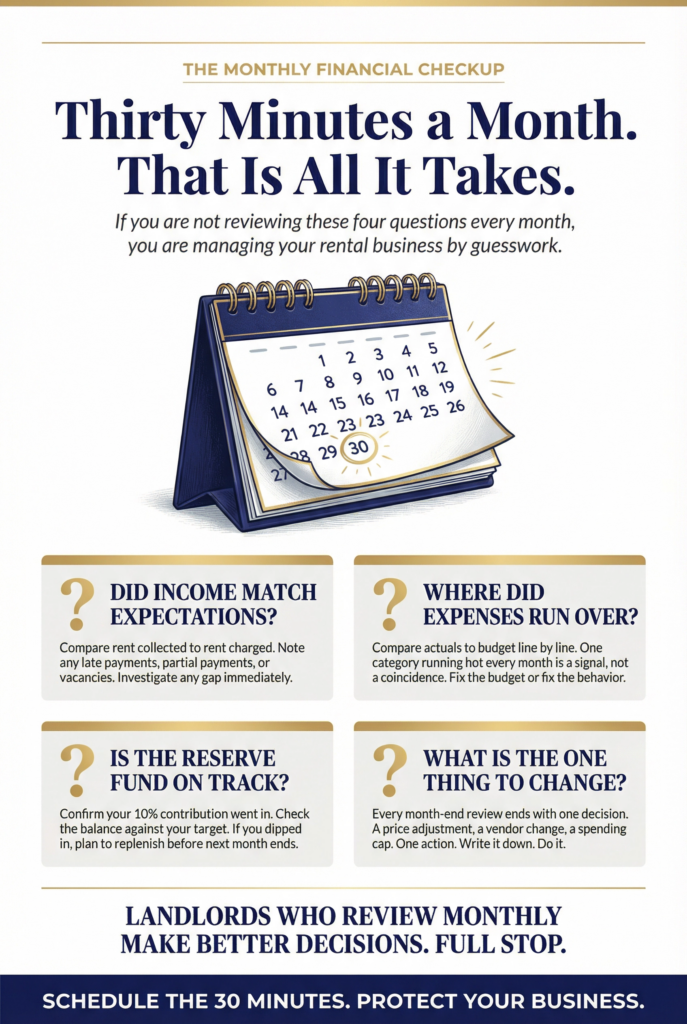

Pick one day each week to review what came in, what went out, and what is pending in the next 14 days. Confirm rent collected, log any new expenses immediately, and flag upcoming bills or renewals so nothing surprises you. End by deciding one action for the week, like scheduling a repair or adjusting your spending cap. - 4. Keep records clean with a simple rule set

Store every receipt and invoice in one place, then record each transaction with a date, vendor, property, and category. Use one consistent chart of categories across all units so your reports stay comparable month to month. Reconcile your bank statements monthly so your books match reality, not memory. - 5. Review monthly results and make one adjustment

Compare actuals vs. budget and note where you were over or under, then update next month’s plan. If a line item keeps running hot, raise your reserve contribution or tighten approval rules for non-urgent spending. This is how your numbers stay useful for decisions like rent changes, renewals, and timing bigger projects.

Keep Rental Books Current with Landlord Accounting Tools

Independent landlords do not usually struggle with effort. They struggle with consistency. A landlord bookkeeping tool matters because it keeps income and expenses organized while you are busy handling tenants, repairs, and renewals.

A practical option is TurboTenant’s recommendations for real estate accounting software that can streamline all of your accounting so transactions get captured, categorized, and ready for reports. That means faster month-end reviews, cleaner tax prep, and fewer missed deductions.

For example, when a plumber invoice hits, you log it once and tag the right property, then your profit picture updates immediately. Once your data is reliable, the next step is answering the common finance questions that still trip landlords up.

Money Questions Landlords Ask Most

Q: What are the key financial skills every landlord should develop to manage rental properties successfully?

A: Focus on four basics: cash flow forecasting, clean expense categorization by property, reserve planning, and reading a simple income statement and balance sheet. Get comfortable with tax compliance habits like saving receipts, documenting repairs versus improvements, and tracking mileage. If you can explain last month’s profit in two minutes, you are in control.

Q: How often should landlords review their financial reports to avoid feeling overwhelmed or confused?

A: Use a light weekly check for rent collected and bills due, then do a deeper monthly close to reconcile accounts and review property performance. Add a quarterly review for taxes, insurance, and reserves so surprises stay small. A fixed cadence beats a marathon catch-up.

Q: What are some effective ways to keep rental property finances well organized and stress-free?

A: Separate banking per business and keep every transaction tied to a property and category the same day it happens. Create a one-page “finance checklist” for month-end: reconcile, review arrears, update reserves, and file receipts. Also keep a running list of deductible upgrades since retrofits may qualify for a rental tax deduction when you meet the rules.

Q: Which types of software tools can simplify financial tracking for landlords without requiring advanced expertise?

A: Look for tools that import transactions, learn categories, store receipts, and generate basic owner-ready reports. The best options also let you tag each charge to a unit and export clean summaries for your tax preparer. If setup takes more than an hour, it is probably too complex for consistent use.

Q: What steps can I take if I feel stuck or uncertain about managing my rental property finances and want to build stronger leadership and management skills?

A: Start by identifying your gap: is it budgeting, bookkeeping, taxes, or decision-making under uncertainty. A structured class can give you a repeatable system, and options like rental property management fundamentals can build confidence fast. If you want deeper oversight, consider earning an MBA online to strengthen finance, operations, and leadership.

Build Rental Business Growth With Monthly Financial Checkups

Rental income can look fine on paper while leaks hide in sloppy records, missed deductions, and emotional decisions. The fix is a simple mindset: treat your rentals like a business, follow financial best practices, and keep ongoing financial learning in motion so your numbers stay honest. Do that consistently and landlord financial decision-making gets faster, calmer, and more accurate, which is how maximizing rental profitability actually happens. If you don’t review the numbers monthly, you’re managing by guesswork. Set a 30-minute monthly money checkup on your calendar to review income, expenses, reserves, and what you’ll change next month. That cadence builds resilience and keeps your rental business growth steady even when the market gets noisy.

{kind=link}